Cross-Border Payouts: How Businesses Move Money Across Markets

Cross-border payouts are payments sent from a business in one country to recipients in another country, usually to contractors, suppliers, creators, affiliates, sellers, or business partners. They sound simple until the money has to cross currencies, banking systems, compliance checks, holidays, and the occasional correspondent bank that appears to operate on geological time.

For a company expanding internationally, payouts are not just a finance function. They shape how fast partners get paid, how predictable cash flow becomes, how much money disappears into foreign exchange spreads, and how much operational work the finance team has to absorb.

What are cross-border payouts?

Cross-border payouts are business payments made to recipients located in other countries. They can include payments to freelancers, marketplace sellers, gig workers, vendors, affiliates, distributors, insurance claimants, or payroll-adjacent workers who are not on a domestic payroll system.

The key difference between a domestic payout and an international payout is the number of systems involved. A domestic bank transfer usually moves through one local payment network. A cross-border payment may involve the sender’s bank, a payment provider, foreign exchange conversion, correspondent banks, local clearing systems, the recipient’s bank, and compliance screening along the way.

That chain matters because every extra party can add cost, delay, or uncertainty.

A company that pays ten local vendors can often handle payments manually. A company that pays 2,000 contractors across 40 countries needs something more structured. That is why finance and operations teams increasingly treat cross-border payouts as payment infrastructure rather than a back-office afterthought.

The money has to arrive. The recipient has to know it arrived. The business has to prove why it moved.

Why do cross-border payouts matter more in 2026?

Cross-border payouts matter more because modern businesses are less domestic than their org charts suggest. A software company may hire engineers in Poland, run customer support from the Philippines, pay creators in Brazil, use suppliers in Turkey, and sell to customers in the Gulf.

The old payment model was built around banks, invoices, and patience. The new operating model is built around platforms, remote teams, marketplaces, affiliate networks, and near-real-time expectations.

That creates pressure in four places:

- Speed – recipients expect payment in hours or days, not vague “processing windows.”

- Cost – FX spreads, transfer fees, and intermediary fees can make small payouts uneconomical.

- Transparency – businesses need to know where a payment is and why a fee was charged.

- Compliance – payments must pass sanctions, anti-money laundering, tax, and identity checks.

The Financial Stability Board has repeatedly pointed to high costs, slow settlement, and poor transparency as core problems in international payments. That is not exactly breaking news to anyone who has ever tried to reconcile a missing supplier payment on a Friday afternoon.

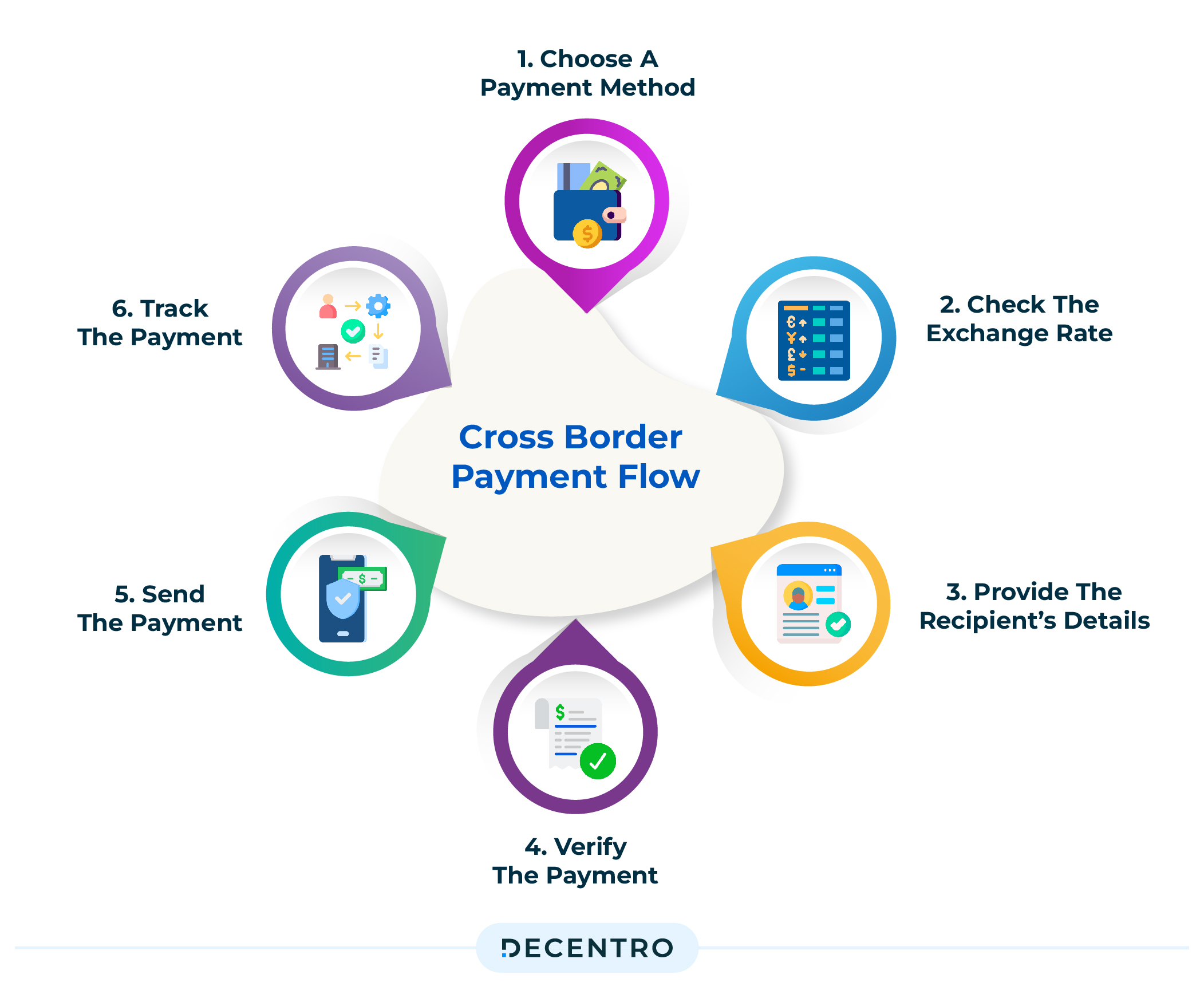

How do cross-border payouts actually work?

Cross-border payouts usually work through a combination of payment rails, currency conversion, compliance checks, and local delivery methods. The exact path depends on the country pair, currency, recipient type, amount, and provider.

A typical payout flow looks like this:

- The business initiates the payment.

- The provider checks recipient details and required compliance information.

- The payment is converted into the recipient’s currency, if needed.

- The money moves through banking or payment rails.

- The recipient receives funds through a bank account, wallet, card, or local payment method.

- The business receives confirmation, reporting data, and reconciliation records.

The rails can vary. Some payments move through SWIFT and correspondent banks. Some use local bank transfer networks. Some providers use card rails, digital wallets, real-time payment systems, stablecoins, or local payout partners.

The important point is that “cross-border payout” is not one single technology. It is an outcome: a recipient in another country gets paid. The path behind that outcome can be clean, expensive, slow, elegant, or a spreadsheet wearing a trench coat.

What makes cross-border payouts difficult?

Cross-border payouts are difficult because payment systems were not designed as one global machine. They were built country by country, regulator by regulator, bank by bank.

The main problems are usually predictable.

Currency conversion

If a company earns in dollars but pays in pesos, euros, dirhams, or lira, someone has to convert the money. The visible transfer fee may be small, while the real cost hides in the FX spread.

That is where many businesses lose more than they expect. A 1% or 2% spread looks harmless on one payout. Across thousands of payments, it becomes a budget line with excellent camouflage.

Intermediary banks

Traditional international transfers may pass through correspondent banks before reaching the recipient. Each intermediary can add time, fees, and failure points.

This is especially painful when the business cannot clearly see where the payment is stuck. “Pending” is not a status. It is a mood.

Local banking rules

Every market has its own banking formats, account identifiers, document requirements, cut-off times, and holidays. A payout that works smoothly in the UK may fail in Indonesia because the recipient name does not exactly match the bank record.

At small scale, finance teams fix these problems manually. At large scale, manual fixing becomes the product nobody meant to build.

Compliance and screening

Businesses must screen recipients, monitor suspicious activity, check sanctions exposure, and collect information required by local regulations. This is not optional.

The difficulty is balancing compliance with user experience. Too little checking creates legal and financial risk. Too much friction delays legitimate payments and annoys the people the business is trying to pay.

Which businesses need cross-border payout infrastructure?

Cross-border payout infrastructure is most useful for companies that pay many recipients in multiple countries. The need becomes stronger when payments are frequent, time-sensitive, or operationally important.

Common examples include:

- Marketplaces paying sellers

- Creator platforms paying influencers and content producers

- Affiliate networks paying publishers

- Gaming and betting companies paying partners or winners where permitted

- Fintech companies moving funds to end users

- Travel platforms paying hosts or service providers

- SaaS companies paying international contractors

- Exporters and importers paying suppliers

- Insurance companies paying claims abroad

- Payroll and employer-of-record platforms handling distributed workforces

A company can survive with manual transfers when international payouts are occasional. It cannot scale that way when payouts become part of the product experience.

If a marketplace pays sellers late, sellers leave. If a creator platform charges too much to withdraw earnings, creators complain publicly. If a contractor waits two weeks for payment, the contractor does not admire the complexity of global banking. They send a follow-up email with a subject line that gets progressively less friendly.

What should companies check before choosing a payout provider?

Companies should check coverage, payout methods, fees, FX transparency, compliance support, reporting, and failure handling before choosing a payout provider. The cheapest-looking option is not always the cheapest operating model.

Country and currency coverage

Coverage should be checked against actual business needs, not a sales page map. A provider may support a country for collections but not payouts, or support payouts only through limited methods.

The practical questions are simple:

- Can we pay recipients in the countries where we operate?

- Can we pay them in local currency?

- Are there minimum or maximum payout limits?

- Are business and individual recipients both supported?

- Are there restricted industries or recipient types?

A map with many shaded countries is useful. A successful test payout is better.

Payout speed and reliability

Speed should be measured by the time it takes for the recipient to actually receive usable funds, not just the time it takes for the sender to initiate the transfer.

A payment marked “sent” may still be moving through intermediaries. For the recipient, that distinction is academic. Their money is either available or it is not.

Businesses should ask for expected settlement times by market and payout method. They should also ask what percentage of payments fail, why they fail, and how failures are resolved.

FX and fee transparency

A serious payout setup should make fees and exchange rates visible before the payment is sent. Hidden FX costs are one of the easiest ways for international payouts to become expensive without looking expensive.

Companies should compare:

- Fixed payout fees

- Percentage-based fees

- FX spreads

- Intermediary bank fees

- Recipient-side fees

- Monthly platform fees

- Refund and failed-payment charges

The invoice may say “free transfer.” The exchange rate may be quietly laughing.

Compliance and risk controls

The provider should support sanctions screening, KYC or KYB workflows where needed, transaction monitoring, audit logs, and documentation. This is especially important for regulated sectors, high-risk corridors, or businesses paying large recipient networks.

The business still owns its risk. Outsourcing payment operations does not outsource accountability.

Reporting and reconciliation

Cross-border payouts create accounting complexity. The business needs clean records for payment status, recipient identity, amount sent, amount received, currency conversion, fees, timestamps, and failed transactions.

Good reporting is not cosmetic. It reduces finance workload, speeds up month-end close, and helps teams answer the most common operational question in payouts: “Where did this money go?”

Are stablecoins changing cross-border payouts?

Stablecoins are changing part of the cross-border payout conversation, but they are not a universal replacement for banking rails. They can make settlement faster and reduce some intermediary friction, especially for businesses moving funds across markets with weak banking access or high FX friction.

The appeal is obvious. A dollar-linked stablecoin can move across blockchain networks faster than many traditional bank transfers. For some payment firms, fintech platforms, and emerging-market use cases, that is not theory. It is already part of their payment stack.

But stablecoins introduce their own questions: regulation, wallet custody, off-ramp liquidity, counterparty risk, blockchain fees, sanctions controls, and user education. A payout is not complete when a token moves. It is complete when the recipient can use the value.

That last step is where many elegant payment diagrams meet the real world.

What is the future of cross-border payouts?

The future of cross-border payouts is likely to be multi-rail. Banks, fintech providers, real-time payment systems, card networks, local wallets, tokenized deposits, and stablecoins may all coexist because different payment corridors have different problems.

The direction is clear even if the winning rails are not. Businesses want faster settlement, lower visible and hidden costs, better tracking, stronger compliance, and fewer failed payments.

Regulators want safer systems, better data, and less financial crime. Recipients want to be paid on time without becoming unpaid beta testers for someone else’s infrastructure.

The best payout systems will probably not be the ones that sound the most futuristic. They will be the ones that make international payments feel boring, predictable, and auditable.

In finance, boring is underrated. It usually means the money arrived.