Keeping Track of Subscriptions and Trial Offers

The Quiet Drain on Your Bank Account

Subscriptions rarely feel expensive in the moment. Ten dollars here. Fifteen there. A free trial that promises to cancel itself if you decide it is not worth it. Each charge seems small enough to ignore.

But over time, those quiet withdrawals add up. Forgotten streaming services, fitness apps you stopped using, software trials that rolled into paid plans without much notice. That slow leak can create real financial pressure. In some cases, it contributes to short term cash shortages that push people to look for fast solutions like a bad credit car title loan.

The irony is that these situations often begin with something marketed as convenient or even free.

Tracking subscriptions is not just about saving a few dollars. It is about protecting your cash flow from silent erosion.

Why Subscriptions Slip Through the Cracks

Modern billing systems are designed to be frictionless. Once you enter your card information, payments continue automatically. That convenience is intentional.

Many companies rely on the fact that customers will forget. The Federal Trade Commission has published guidance on subscription and negative option billing practices, noting that consumers are often charged after free trials end if they do not actively cancel.

The problem is not always deception. It is distraction.

You sign up during a busy week. You tell yourself you will evaluate it later. Months pass. The charge blends into your statement, just another line item among many.

Without a system for tracking these commitments, they multiply quietly.

Cancel First, Decide Later

One of the most effective habits you can build is scheduling cancellation immediately after signing up for a trial.

It sounds counterintuitive, but many services allow you to cancel right away while retaining access until the end of the trial period. That means you still get the benefit of the full trial, but you eliminate the risk of forgetting.

If you decide the service is worth keeping, you can always re subscribe before the end date.

This approach flips the default. Instead of relying on memory, you rely on automation.

Set a calendar reminder for a few days before the trial ends. Or cancel immediately and remove the pressure entirely. Either way, you stay in control.

Use Technology to Monitor Technology

Just as subscriptions are automated, tracking them can be automated too.

Several budgeting and financial management apps scan your bank transactions and flag recurring charges. They categorize subscriptions, estimate monthly totals, and send reminders when trial periods are ending.

While no tool is perfect, these apps create visibility. Seeing all your recurring expenses listed in one place can be eye opening.

Even if you prefer not to use an app, your bank’s online dashboard may offer recurring payment tracking features. Explore what tools are already available through your financial institution.

Visibility is the first step toward control.

Review Statements Like an Investigator

Even with tracking tools, monthly statement reviews are essential.

The Consumer Financial Protection Bureau recommends reviewing bank and credit card statements regularly to identify errors, unauthorized transactions, or forgotten charges. This habit not only helps with subscriptions but also protects against fraud.

Approach your statement with curiosity. Do you recognize every charge? Are there services you no longer use? Have prices increased quietly over time?

Subscription costs often creep upward. A service that started at nine dollars per month might now cost fifteen. Those incremental increases are easy to miss without intentional review.

Make this a routine. Schedule it on the same day each month so it becomes automatic.

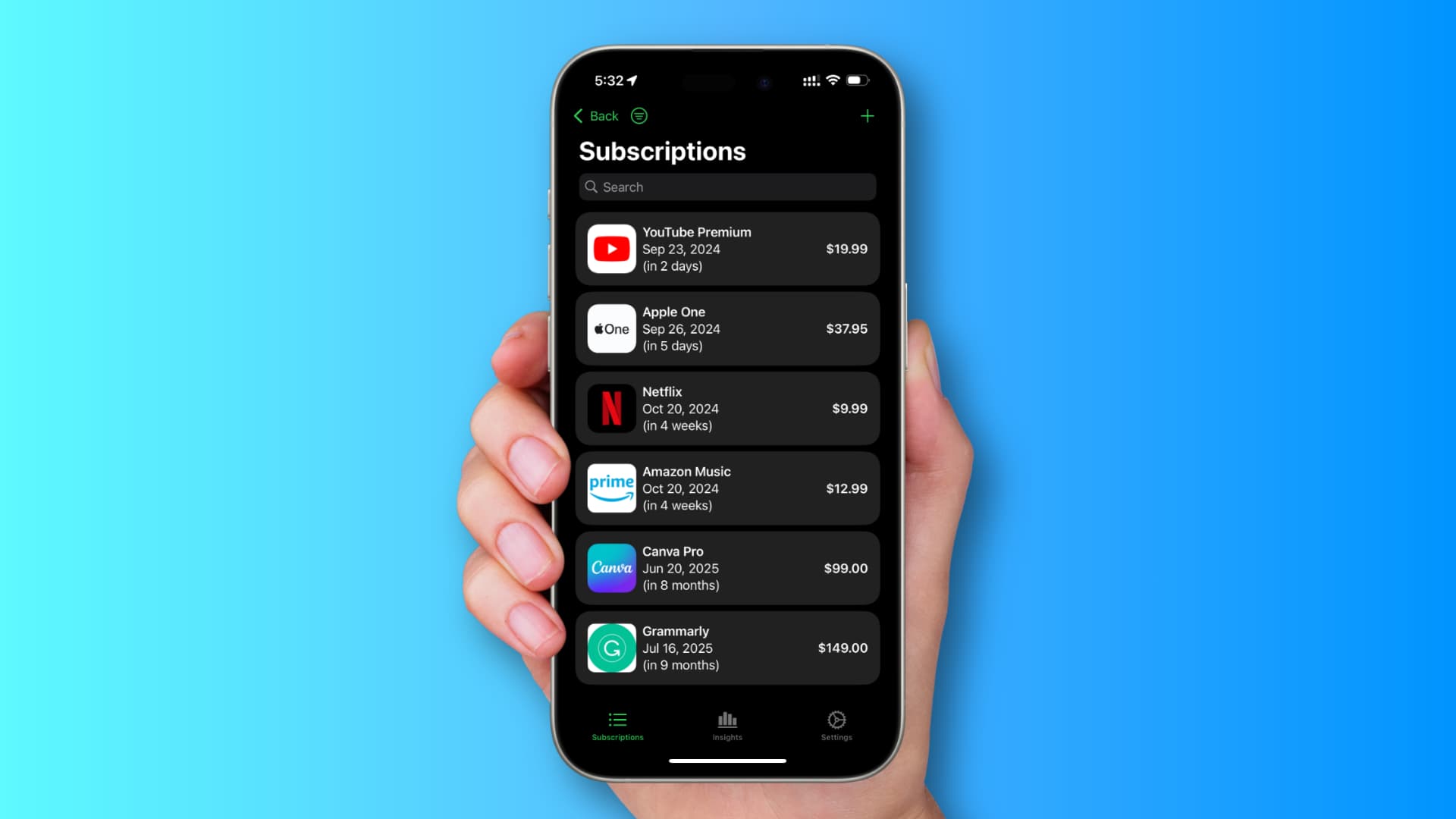

Create a Subscription Inventory

Instead of relying solely on transaction history, create a simple inventory of all active subscriptions.

List the service name, monthly cost, renewal date, and cancellation method. This document does not need to be complex. A basic spreadsheet works fine.

Seeing the total monthly subscription cost in one number can change your perspective. What felt like small, isolated charges may represent a significant portion of your discretionary spending.

An inventory also makes cancellation easier. You know exactly where to go and what steps to take.

Differentiate Value from Habit

Not all subscriptions are wasteful. Many provide genuine value. Streaming platforms, educational services, productivity software, and wellness apps can improve quality of life.

The key question is whether you are paying out of habit or purpose.

Every few months, review your subscription inventory and ask yourself whether each service still aligns with your needs. If you would not sign up for it today at its current price, that is a sign it may no longer fit.

This mindset keeps your spending intentional rather than passive.

Watch for Bundling and Annual Billing

Some companies encourage annual billing by offering discounts. While this can save money, it also increases the risk of forgetting about the service entirely.

Before committing to annual plans, evaluate whether you truly use the service consistently. If your usage fluctuates, a monthly plan may offer more flexibility even if the per month cost is slightly higher.

Bundled subscriptions also deserve attention. A single platform may include multiple add ons or premium tiers. Review what you are actually using and adjust accordingly.

Small Leaks, Big Impact

Individually, most subscriptions will not break your budget. But collectively, they can shape your financial landscape.

If you free up fifty or one hundred dollars per month by eliminating unused services, that money can strengthen your emergency fund, reduce debt, or support long term savings.

Over a year, those small adjustments add up significantly.

Keeping track of subscriptions is not about being overly restrictive. It is about ensuring your money reflects your priorities.

Build a Habit of Active Oversight

The digital economy thrives on recurring payments. Convenience is the selling point. But convenience requires counterbalance.

By canceling trials proactively, using tracking tools, reviewing statements monthly, and maintaining a clear inventory, you shift from passive participant to active manager.

Your bank account should not be a mystery. When you know exactly where your money is going, surprise charges lose their power.

Subscriptions and trials do not have to be financial traps. With a few consistent habits, they become choices you control rather than expenses that control you.