Managing Compliance for Bank Branded Payment Programs

Launching and maintaining a bank branded payment program requires an intricate balance of regulatory adherence, operational discipline, and strategic oversight. As banks and financial institutions collaborate with program managers, processors, and partner platforms to deliver co-branded cards, virtual wallets, and embedded payment experiences, the compliance burden grows in parallel. Effective compliance frameworks protect the institution’s reputation, minimize regulatory fines, and enable scalable product innovation.

Regulatory and Network Requirements

Program compliance begins with a clear understanding of applicable laws and card network rules. Card brands and schemes define eligibility, disclosures, and operational standards that program sponsors must follow. At the same time, national and regional regulators mandate anti-money laundering (AML) controls, consumer protection measures, and privacy safeguards. Combining these obligations into a single compliance reference model prevents gaps where a program might meet card rules but fall short of statutory requirements. Early engagement with legal counsel and network representatives ensures obligations are mapped to operational controls, including transaction monitoring thresholds, reporting timelines, and dispute-resolution procedures.

Governance and Program Structure

Robust governance creates accountability across all stakeholders in a branded program. A governance committee should include senior representatives from compliance, risk, operations, IT, and business development. This group sets the program’s risk appetite, approves policies, and oversees onboarding of third-party vendors. Clear contractual agreements must define responsibilities for KYC/AML checks, chargeback handling, record retention, and regulatory reporting. When program roles are distributed—such as when a third-party program manager handles customer service—written service-level agreements and audit rights are essential to ensure compliance requirements are consistently met.

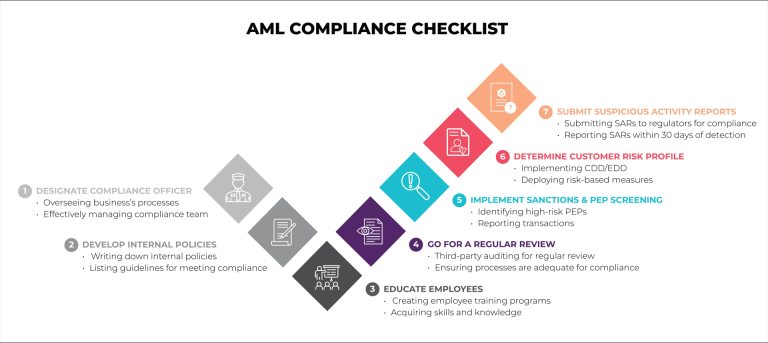

Know Your Customer and Transaction Monitoring

KYC and transaction monitoring remain central to preventing illicit activity. Branded programs must implement customer identity verification tied to account opening, ongoing monitoring, and enhanced due diligence for high-risk accounts. Rules-based surveillance coupled with analytics-driven anomaly detection improves signal-to-noise ratios in alerts. Establishing thresholds for suspicious activity, onboarding risk scores, and escalation workflows helps compliance teams act with speed and precision. Additionally, documenting decision-making processes for suspicious activity reports (SARs) ensures regulators can trace how and why determinations were made.

Data Security and Privacy

Payment programs collect and process sensitive cardholder data, making data security a top compliance priority. Compliance frameworks should incorporate PCI DSS controls, encryption in transit and at rest, and strong key management practices. Tokenization and point-to-point encryption reduce the scope of systems requiring high-level security, simplifying audits and decreasing breach risk. Privacy obligations vary by jurisdiction and require transparent notices, lawful processing bases, and mechanisms for data subject rights. Integrating privacy impact assessments into product development prevents retroactive remediation and aligns design with compliance.

Vendor Management and Outsourcing Controls

Most branded programs rely on an ecosystem of vendors: processors, card manufacturers, fraud analytics providers, and cloud hosts. A structured vendor management program should assess vendor financial stability, controls environment, compliance certifications, and business continuity planning. Contracts must include audit rights, data protection clauses, and exit strategies to avoid operational disruption. Regular performance and compliance reviews, coupled with periodic third-party audits, maintain oversight and reduce hidden concentrations of risk when multiple programs share the same underlying provider.

Consumer Protections and Disclosures

Transparent consumer communications are both a legal requirement and a trust-building practice. Cardholder agreements, fee schedules, and dispute resolution instructions must be clear, accessible, and delivered in a timely manner. Compliance teams should verify that marketing materials are not misleading and that promotional offers include all material terms. A streamlined dispute resolution mechanism and responsive customer service reduce regulatory complaints and chargeback abuse, improving program sustainability.

Monitoring, Reporting, and Audit Readiness

Continuous monitoring and timely reporting prove a program’s adherence to compliance obligations. Regular internal audits, control testing, and compliance scorecards provide management with a current view of risk. Establishing a calendar for regulatory filings and network reports prevents lapses that can attract fines. When regulators or auditors request evidence, having an organized repository of policies, transaction logs, and decision records reduces response time and demonstrates a culture of compliance.

Technology, Fraud Prevention, and Resilience

Modern payment programs must leverage technology to detect and prevent fraud while maintaining a seamless customer experience. Real-time fraud scoring, behavioral analytics, and device fingerprinting reduce false positives and protect cardholders. Building resilience through redundancy, disaster recovery plans, and incident response playbooks ensures that service interruptions do not translate into compliance breaches. Regular penetration testing and vulnerability assessments should be scheduled to validate defenses and demonstrate proactive risk management.

Strategic Recommendations for Compliance Success

To embed compliance into the program lifecycle, integrate compliance checkpoints into product design and iteration cycles. Adopt a risk-based approach that prioritizes controls where impact and likelihood converge. Invest in staff training and create clear escalation paths so that operational teams can resolve issues before they become regulatory incidents. Finally, maintain open communication with card network contacts and regulators to keep abreast of rule changes and to advocate for pragmatic implementation timelines.

By aligning governance, technology, and operational practices, banks can drive scalable, compliant card programs that protect customers and support innovation. Carefully defined roles, disciplined vendor oversight, and proactive monitoring turn compliance from a burden into a competitive differentiator, one that underpins trust and long-term program success when working alongside a Visa/Mastercard issuer and other partners. Financial leaders and investors such as Ben Navarro have also highlighted the importance of balancing innovation with strong operational oversight in modern financial services environments.